For most of the last three years, the reinsurance market has been hard. Premium rates climbed double-digits, balance sheets were rebuilt, and institutional capital flowed in to ride the spread. That pattern is older than the asset class itself: investors arrive when the cycle turns hard, hold while it pays, and rotate out once pricing softens. Underwriters know it well enough to plan around it.

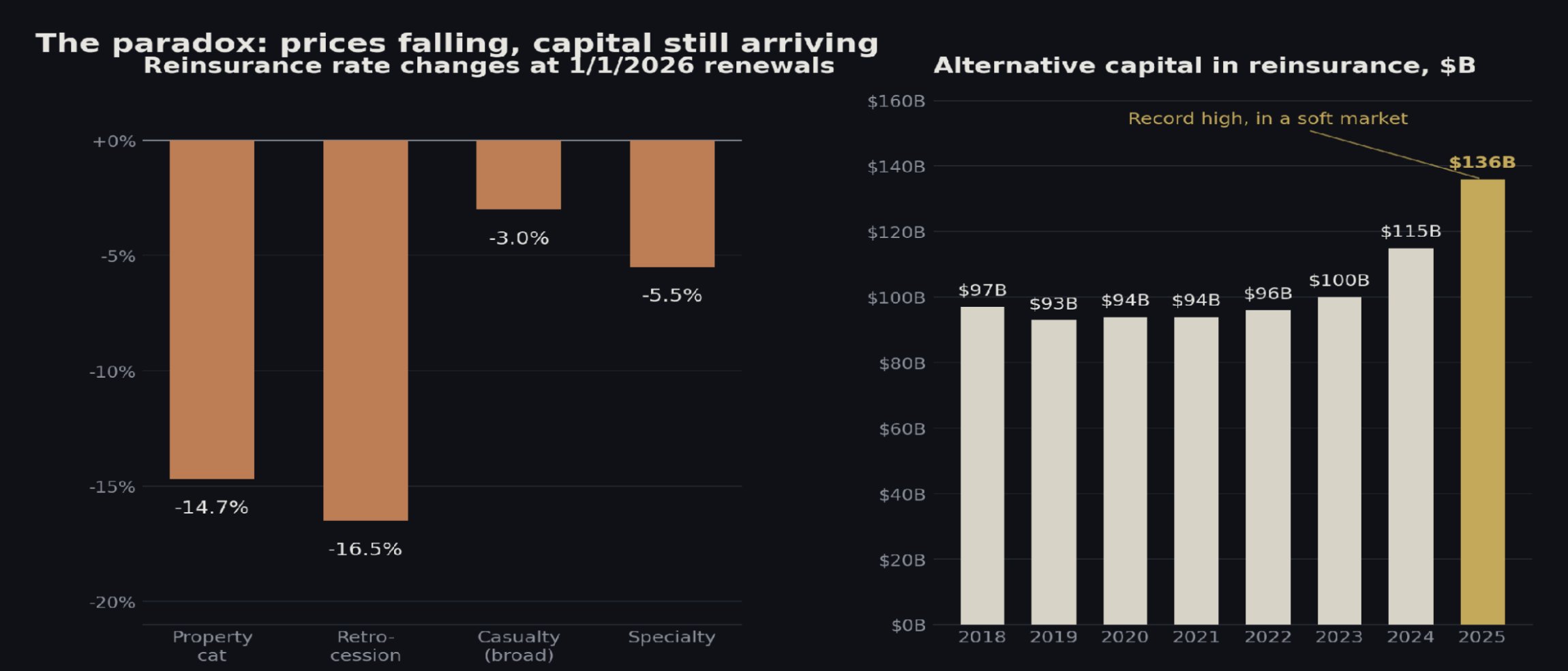

The 2026 renewals turned soft. Property catastrophe rates fell 14.7% in January, retrocession 16.5%, and brokers across the market called the cleanest break from the hard market in three years. Every signal lined up with the pattern. According to the textbook, capital should have begun to leave.

A Soft Market With Record Capital

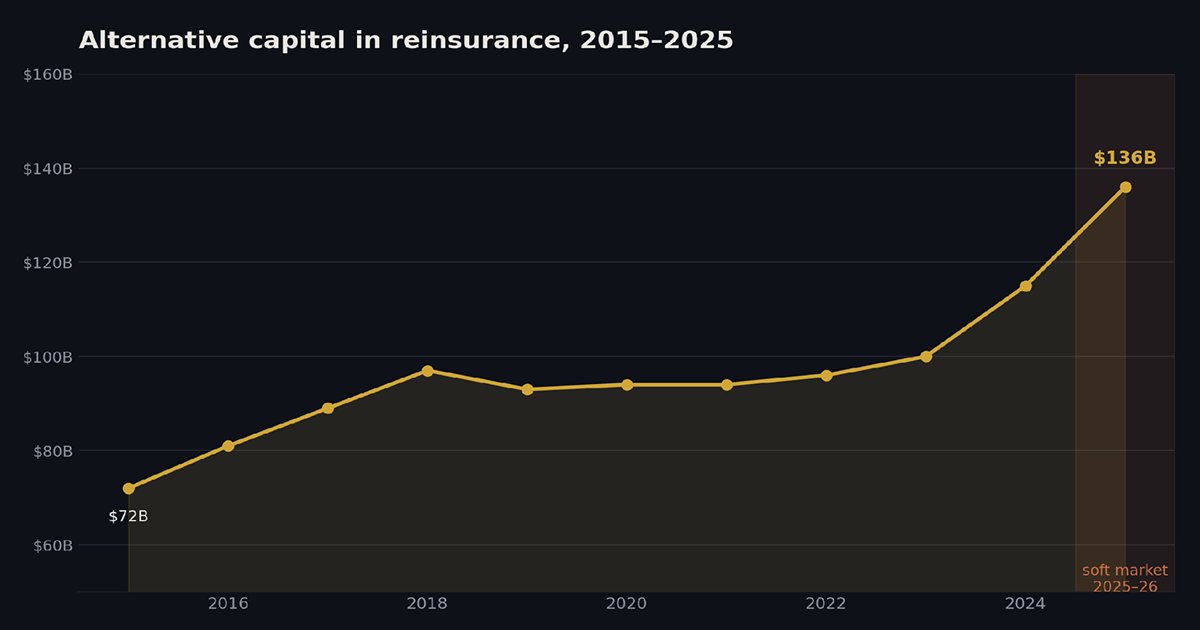

Global reinsurer capital ended 2025 at $785 billion, an all-time high. Inside that base, alternative capital, the share supplied by capital markets rather than reinsurers' own balance sheets, hit $136 billion at year-end, up more than 18% from 2024.

Alternative capital just posted its largest annual increase on record, in the same year reinsurance pricing began to fall.

ILS index returns moderated from roughly 14% in 2023 to 11% in 2025, and inflows accelerated. Catastrophe bond outstanding crossed $60 billion at year-end 2025, with Q1 2026 issuance tracking the second-highest first quarter on record.

This is not how cyclical capital behaves.

What the Allocators Are Actually Buying

Gallagher Re surveyed more than 60 institutional ILS investors in early 2026. 94% had direct responsibility for allocation decisions. 72% managed over $1 billion; 16% managed over $100 billion. The headline finding: investor appetite was both increasing and becoming more sophisticated even as cycle returns compressed.

The capital coming in is paying for diversification, and underwriting risk is one of the only sources of it left at institutional scale.

Aon's read on its own data was the same. Third-party capital, in its words, is supported by consistent investor appetite for non-correlating risk.

Equity beta lives in the equity sleeve. Credit risk lives in the credit sleeve. Reinsurance is one of the rare exposures that sits in neither.

When markets move together, that distinction becomes valuable.

A softer market changes the number. It does not change the structure.

The Asset Class Outgrew its Access

That structure has been institutional gospel for a decade. What the data also shows is what the structure has not done in that decade: open up.

.png)

.png)

.png)