For most of the last cycle, yield in crypto meant one thing. A protocol printed a token, paid it to depositors, and called the number a yield. It showed up in a wallet, so it felt real, and nobody asked how long it would last because new capital arrived faster than tokens were printed.

That window has closed, and the numbers leaving the system don't leave much room for argument about why.

The market has already moved

DeFi TVL: $170B to $98B between October 2025 and late February 2026. Average stablecoin yield on the largest lending protocols now sits below 2% APY, the lowest level since 2023, while the 10-year US Treasury pays 4.24%.¹

DeFi now pays less than Treasuries.

Capital is leaving speculative yield pools for foundational layers. Liquid staking holds roughly 40% of the remaining DeFi TVL.¹ Token emission schedules across major protocols are mechanically declining, and 77% of DeFi yield in 2024 already came from real fee revenue rather than emissions.²

The trade stopped being profitable, which is a harder problem to fix than going out of fashion.

The math nobody wanted to do

The economics were always there, just easy to ignore while prices went up.

A token printed to attract liquidity needs someone to buy it on the other side. Belief buyers are finite, so when they run out, the token falls. Realized yield falls with the token, even when the dashboard APY stays high. Thirty percent on a dashboard is worth far less once the token paying it loses half its value.

When emissions stop, what is left is whatever was underneath, and usually that is not much. A protocol whose only yield is its own token has no yield once the token stops rising, while protocols generating returns from other sources, like fees, premiums, or interest paid by real borrowers, keep producing them.

That difference didn't matter much while everything was going up, but it is now the only thing that does.

The yields that did not survive the test

Some yields outlived emissions, but not all of them are what they look like.

Synthetic dollars built on perpetual funding rates produce real cash flow rather than subsidies, but the yield moves with the crypto market structure. Funding rates depend on bullish positioning in perp futures, so when positioning weakens, funding compresses and yields with it. In extended periods of bearish positioning, the strategy can flip from earning funding to paying it.

APYs on this strategy class have ranged from roughly 4% to over 30% across cycles. Supply has collapsed sharply during stress events, most visibly in late 2025, when one major synthetic-dollar protocol lost over $6B in supply during a depeg window.

The strategy is real. The yield is a function of market structure, not an independent one.

Risk got more visible at the same time the yield shrank. It is tempting to say protocols got riskier, but they did not. The risk was always there, just not priced. Crypto theft hit roughly $3.4B in 2025, with Q1 2025 the worst quarter on record.³ A major lending market lost around $6B in TVL within 48 hours of an exploit on a bridge it had no exposure to, because the affected collateral was composable across the stack.

The market spent two years putting a price on the risk it had been carrying for free.

The question changed

The last cycle asked one question: how much does it yield? That number was the whole decision. The next cycle asks three, and none of them are easier:

- Where does the return come from?

- What risk comes with it?

- Who is pricing that risk?

The pivot is straightforward: capital that used to chase the highest number now wants to know where the number comes from.

These are the questions a credit desk asks before allocating, and onchain capital is asking them too, visibly, with capital flows behind it. Crypto vault TVL surpassed $6B in 2025 and is projected to double in 2026,⁴ with a new institutional layer of risk curators emerging to price exposure, set limits, and publish stress-test disclosures.

An academic paper from December 2025 framed the shift bluntly: the main locus of risk in DeFi lending has migrated upward from base protocols to a permissionless curator layer.⁵

Mature financial systems do not remove risk, because there is no finance without risk. They make risk legible, price it correctly, and build the machinery to move it from people who do not want it to people who are paid to hold it.

The shift is not from yield to no-yield. A market that competed on the highest advertised number is becoming a market that competes on how honestly that number is built.

So the question for any yield is no longer how high it is, but what it is made of, and whether the thing it is made of was built to be priced.

The machine that already prices risk

There is an industry whose whole job is pricing and moving risk. It has run for more than three centuries and survived every financial cycle in modern history, because its returns are not a function of any financial cycle.

It is reinsurance.

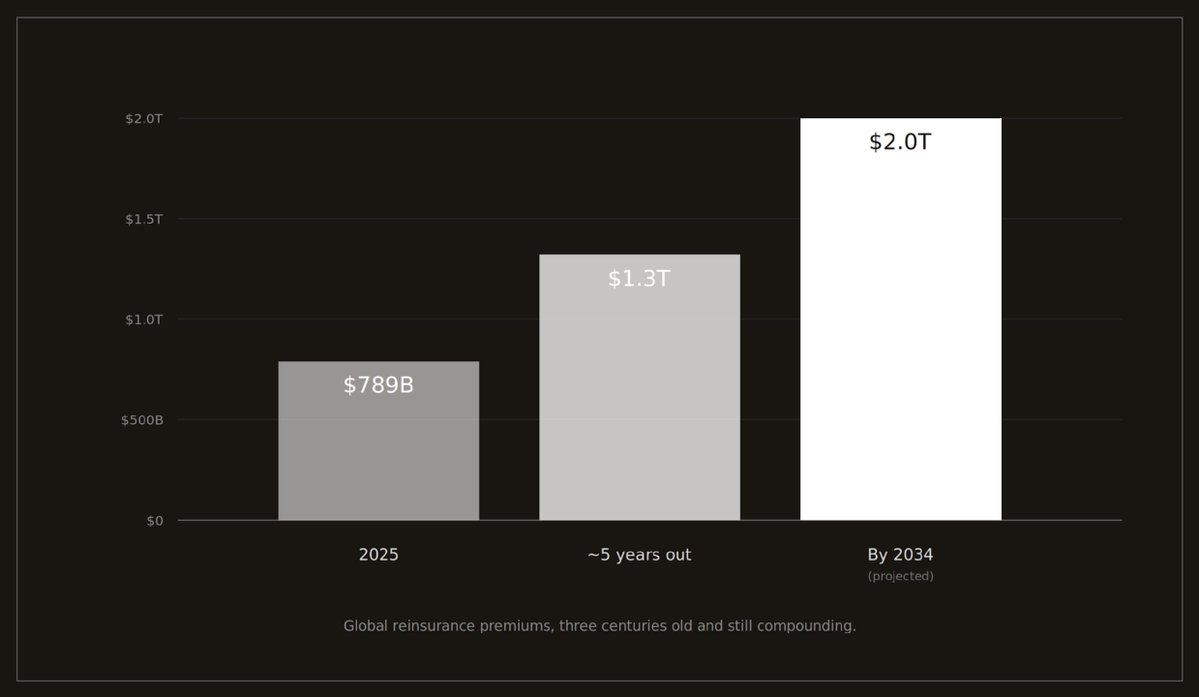

$789B in global premiums by 2025. Projected toward $2T by 2034.

The numbers describe a market operating at full institutional scale. The largest reinsurers posted a record 21.1% average return on equity in H1 2025.⁷ The sector earned returns above its cost of capital for three consecutive years.⁷ Total dedicated reinsurance capital reached $607B in 2025, with alternative capital structures expanding inside it.⁸ Collateralized reinsurance has no public-market exposure, and therefore no market correlation, by structure rather than by claim.

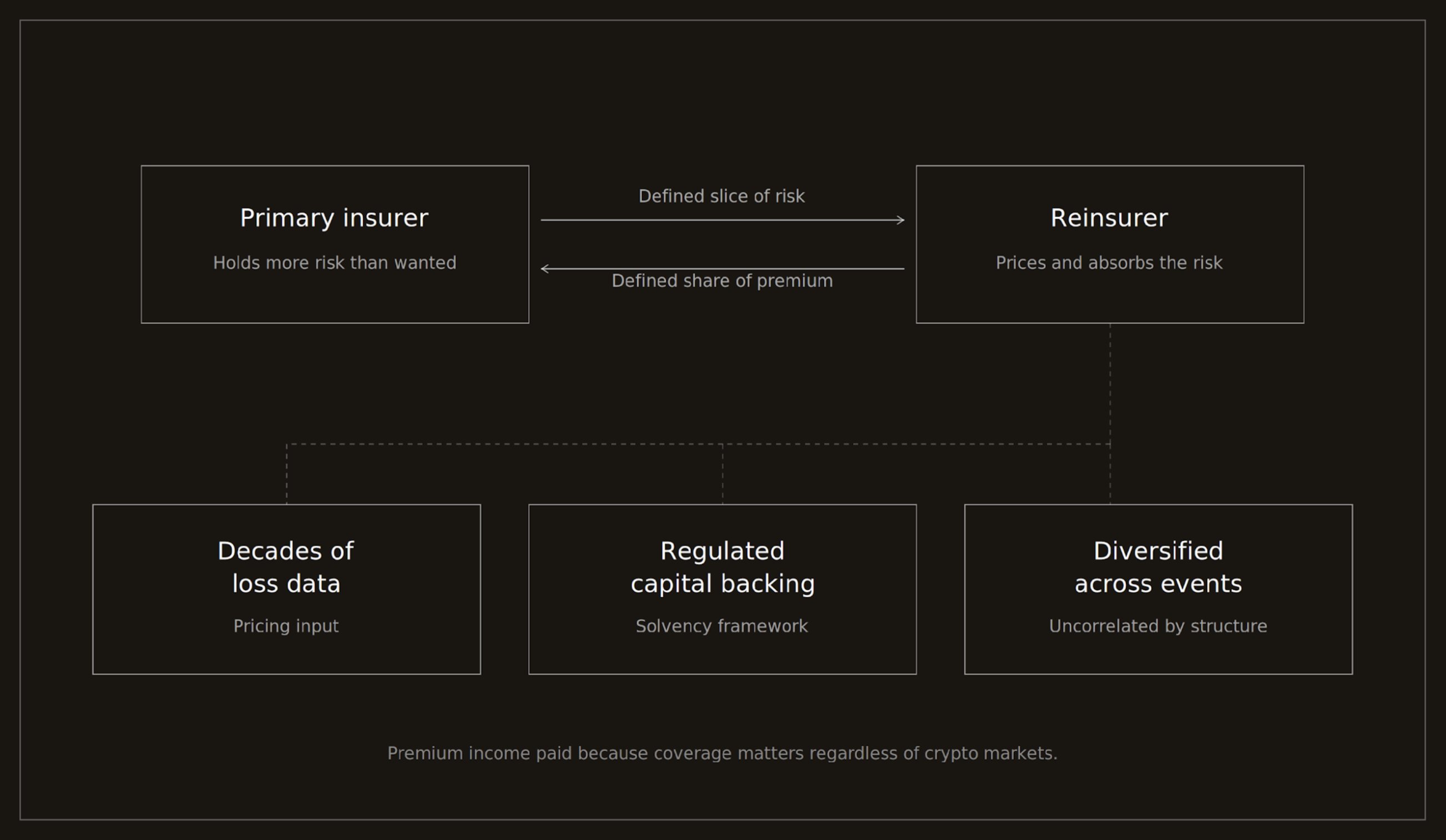

An insurer hands a defined slice of its risk to a reinsurer for a defined share of the premium. The reinsurer prices that risk on decades of loss data, holds regulated capital against it, and spreads it across events that have nothing to do with each other or with markets.

A hurricane doesn't check a token price before it lands, and the insurer still owes the claim, no matter what crypto is doing that month.

For most of its history, this return was out of reach without an institutional letterhead and a large minimum. The barrier was never the asset. It was access, and access required a native form on a system that could custody, settle, and compose it.

That part changed.

Put the same return onchain, inside a regulated structure, as an asset other protocols can hold and use, and it answers the new questions that the market is now asking:

- Where does the return come from? Premiums paid by insurers for real coverage.

- What risk comes with it? Underwriting risk, modeled and capped per contract before any exposure begins.

- Who prices it? The same actuarial and underwriting process that has priced insurance risk for generations.

.png)